The Bank says things are awful

An early-1990s style recession lasting five quarters, the steepest drops in real household income on record, inflation remaining high throughout 2023, rising unemployment and catastrophic rises in energy bills.

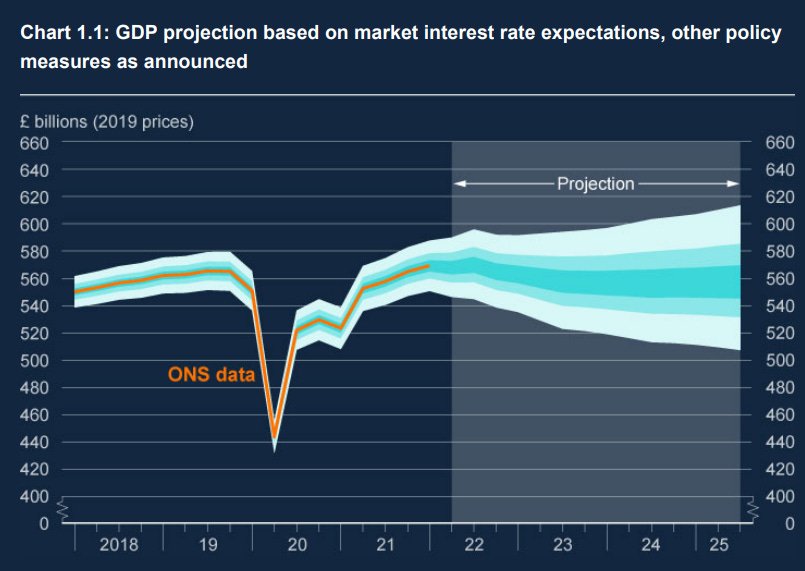

The key charts are below:

GDP contracts and then flatlines, with an historically weak recovery.

Inflation remains at the kind of levels the UK hasn’t experienced in a generation throughout next year.

And unemployment rises throughout the forecast.

Real household incomes suffer an unprecedented hit. The Bank’s forecast produces a fall of 1.5% this year and 2.25% next year. That would be the biggest two year drop since at least the 1940s.

But this forecast is almost certainly wrong

It is vitally important to remember that this forecast assumes no changes in fiscal policy.

And fiscal policy looks set to change as early as next month. Whoever is Britain’s Prime Minister by early September there will be an emergency fiscal event before the end of that month.

Some combination of tax cuts, bill rebates or both will almost certainly be put in place before the October rise in the domestic energy price cap.

That will cushion the blow to real incomes and, perhaps, provide some marginal support for consumption.

Things are going to be get very tough for households, firms and growth but perhaps not quite as bad as this horror show of a forecast implies.

But that’s when things get really tricky

The Bank is currently hiking interest rates into a coming recession. As Chris Giles noted this afternoon, it is hard to avoid the conclusion that the Monetary Policy Committee have decided a recession is necessary to return inflation to target.

The very same politicians who have spent much of the last year berating the Bank’s ‘failure’ to control inflation will not, I suspect, be especially happy with the Bank taking action to control inflation.

I always find it helpful to substitute the phrase ‘control inflation’ with ‘raise interest rates to tighten financial conditions, discourage corporate investment and hiring and slow wage and employment growth”.

The nature of Britain’s inflation

The most interesting analysis in the Report is Box E on international comparisons of inflation.

The cross-OECD picture is a useful reminder that high headline inflation is global in nature.

The Bank further notes that, as expected, energy and food inflation have picked up sharply globally. But when it comes to services and core goods there is some evidence of an Anglo-American vs Euro area divergence (partially offset by Euro area energy price inflation being higher).

Core goods price inflation in the UK was 6.5% in June, higher than the euro area, where it was 4.3%. Some of the strength of goods price inflation in the UK relative to the euro area might reflect a normalisation in price levels. Clothing and footwear prices were particularly low in the UK in 2020 because of discounting in the pandemic; inflation in this component has subsequently been higher than in the euro area. US goods price inflation picked up earlier than elsewhere, reflecting particularly strong demand, especially during the pandemic. Core goods price inflation has been somewhat higher in the UK than the euro area recently. This might reflect some UK prices recovering from unusually low levels in the pandemic. It may also reflect the tighter labour market. Higher goods price inflation in the UK and US compared to the euro area may also reflect labour market tightness. Although services inflation is often assumed to be a clearer indicator of domestic inflationary pressures, almost all goods embody some domestic labour input as well. As a result, higher goods inflation might reflect some of the same drivers of higher services price inflation

The broad brush way to think about this - in terms Andrew Bailey used at a recent press conference - is that Euro area inflation is primarily an energy price story, US inflation is a tight jobs story and British inflation is a bit of both.

Watch the labour market

Almost as interesting as the comparative analysis of inflation dynamics is the deep dive into the labour market in chapter 3.

I really like this chart on labour demand and labour supply.

The basic story is that labour demand recovered much faster from the pandemic than labour supply. The Bank’s analysis of the labour supply story is some I will be returning to next week.

But when it comes to their jobs market outlook, I was struck by the final paragraph:

On the other hand, labour market tightness could unwind more quickly. The labour market may respond more rapidly to slowing demand. Recruiters mentioned that greater economic uncertainty and rising costs were already slowing hiring according to the June KPMG/REC UK Report on Jobs. The Covid-related factors weighing on participation could also unwind faster than assumed in the baseline projections if, for example, the very recent decline in inactivity continues at the same pace over the coming months. Labour supply growth could also be affected by how households respond to the real income squeeze. Households may seek to boost income through working more, which could involve those currently inactive re-entering the labour market or those already in the labour force seeking to work longer hours. Although, if unemployment starts rising, households may become discouraged from entering the workforce as fewer jobs are available.

I’m more pessimistic on the jobs market than the MPC. What they outline as a possibility feels closer to my own base case. If real household income takes a large hit and consumption falls then I can see the current tightness in the jobs market unwinding pretty swiftly indeed. I don’t see labour-intensive consumer facing firms posting anywhere near as many job ads if the Bank’s outlook is even half right. Similarly, although it is a smaller part of the supply story than chronic illness, I can easily see a substantial proportion of the 50- and 60-somethings who chose to retire earlier than planned in 2020 and 2021 rapidly reassessing that decision in the face of a real income shock.

Thanks for reading Value Added. It is a subscriber funded publication. If you’re enjoying it please do consider taking out a subscription. You’ll get more posts and I’ll get the resources to carry on writing it.