Reasons to hike

Reasons to hike

The best argument for Bank of England tightening isn't about inflation expectations. It's because everyone else is doing it.

Yesterday Michael Saunders of the Monetary Policy Committee, who voted for a 0.5% rather than 0.25% increase in Bank Rate last week, set out some of his reasoning.

The whole event at which he spoke is available on Youtube and worth taking the time to watch.

The case for hiking is, of course, straight forward. Whilst the vast majority of the rise in prices that is squeezing household income is being driven by global factors (energy, food and supply chain disruptions), the Bank’s forecasts also show a smaller pick-up in domestically generated inflationary pressure. The kind of inflation that should be controllable by domestic monetary policy.

I am (much) less convinced by the argument Saunders majored on, namely the importance of keeping inflation expectations ‘well anchored’.

Saunders’s speech mentions expectations sixteen times, a sure sign that they are occupying a prominent place in his thinking.

As he put it:

The rise in inflation is already creating spillovers to the economy, including second-round effects on wages and costs. Longer-term inflation expectations measured from households or financial markets have risen further and are uncomfortably high (see figure 7). There are signs that pay deals have picked up markedly this year. The BoE Agents report that the tight labour market is the main driver pushing up pay deals, but the high rate of actual and expected inflation is also a major factor. Business surveys suggest that firms expect to continue to raise their selling prices rapidly, and there is little sign that firms’ pricing strategies are constrained by the 2% inflation target. Uncertainty over inflation has risen, especially among firms affected by supply and labour shortages and in energy-intensive sectors. (My emphasis)

Backed up by a worrying looking chart.

The problem with this argument is that whilst the notion inflation expectations as a driver of long-term inflation is an appealing argument for central bankers, the empirical (and even theoretical) case for this is weak. What’s more, a quick eyeballing of his chart would suggest that UK inflation expectations tend to move with actual experienced inflation rather than foreshadowing it.

Other arguments for hiking are available.

I increasingly think the best case for the BOE hikes is simply that its peers are doing the same.

Whilst I am fond of telling my elder children not to do something just because everyone is, the same logic may not apply to the central bankers of a small, open economy.

It’s worth stepping back and looking at the last twenty or so years of inflation outturns in Britain, the G7 and the OECD.

It is hard to look at such a chart and not conclude that global factors have played a big part in the inflation outcomes of the last two decades.

It is also worth noting that the current below average rates of inflation in the UK mostly reflect the functioning of the retail energy price cap – which means energy price inflation takes longer to feed into the British numbers. The peak British CPI will almost certainly come after that in the US and Europe.

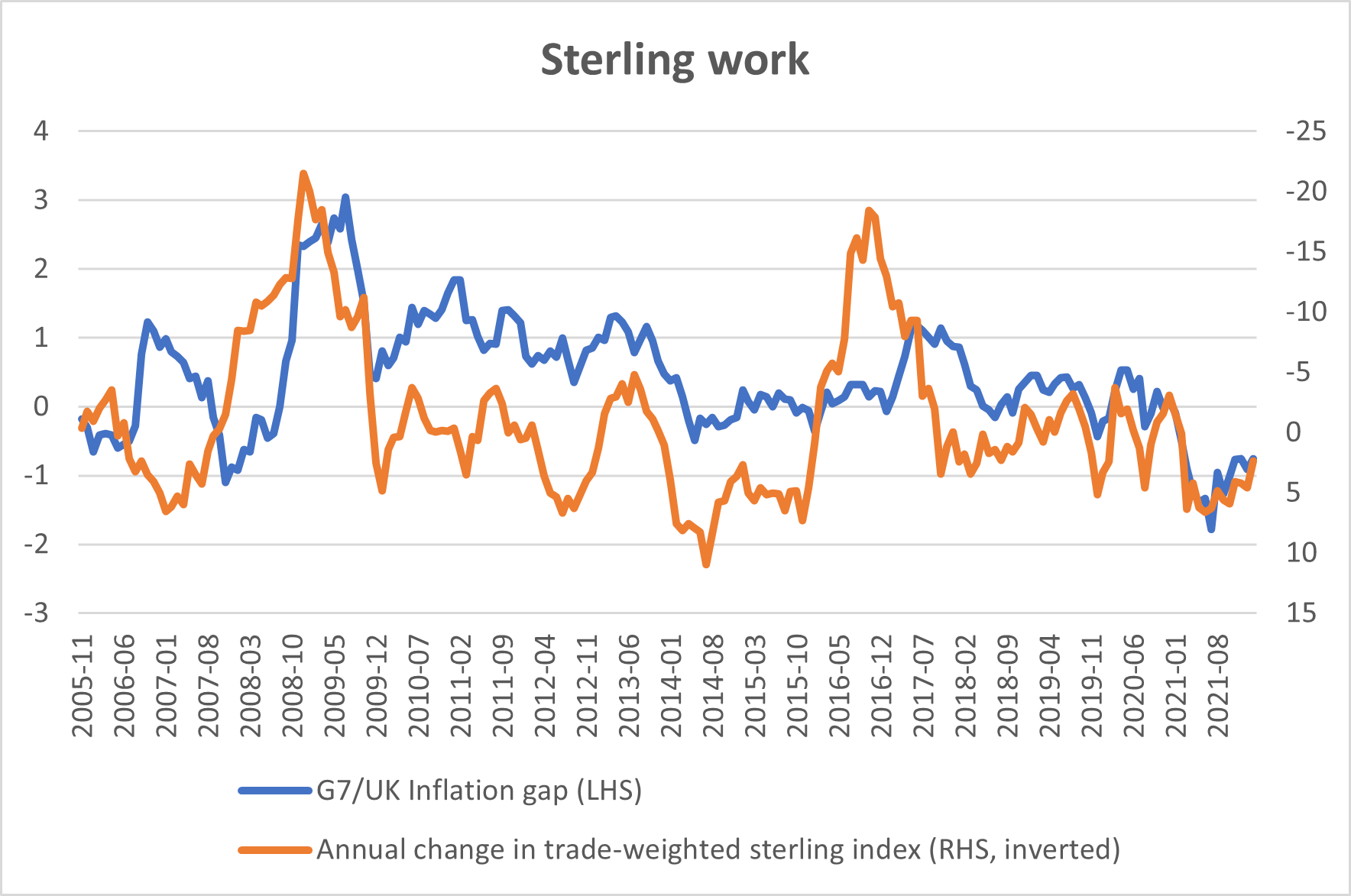

But what I find more useful, is to note the two periods in the last fifteen years or so when British inflation overshot the kind of rates seen elsewhere in the G7 and OECD. The period after 2009 and again in the middle of the 2010s.

Both are sterling stories. The large devaluation after the financial crisis and the big drop in the value of the pound after the Brexit referendum of 2016 were both accompanied by sharp pick-ups in inflation.

The chart below gives an imprecise sense of the relationship:

The Bank of England (and I can almost hear the slightly robotic tone in which this would be said) ‘does not target the exchange rate’. But it is an input into what they do target: inflation at 2%.

And an input they cannot ignore. Threadneedle Street will not have been happy with the reaction to last week’s Monetary Policy Report in the FX market.

The outlook for both British households – and the wider economy – is becoming increasingly grim. Sadly, there is not much the Bank can do about that. As the Governor rather strongly hinted last week, what’s really needed to support households – and ultimately the wider economic outlook – is more help from fiscal policymakers. The ball is in the Chancellor’s court.

Some Plugs:

I’m speaking tomorrow at a fascinating looking Resolution Foundation event on how people perceive the economy and what that means for policy. Sign up here.

And next Tuesday, I’ll be helping the Work Foundation make sense of the latest jobs market figures on a panel. Sign up here.

As a final plug: Muddling Through is out now in paperback. You can buy it from your preferred retailer via that link. Or by going to a shop.

If you’re enjoying Value Added, please do subscribe. You’ll get more posts and I’ll get the resources to carry on producing it.