The Year of the Squeeze

Households are set for a rough year and the government will come under pressure for easier fiscal policy at Spring's budget.

A very Happy New Year to all Value Added readers.

This week the FT published its annual survey of economists’ views on the UK economic outlook. It didn’t make for an especially uplifting read. The broad consensus is that the risks to growth are stacked towards the downside and that high inflation will squeeze real incomes. I find it hard to lean much against either aspect of this consensus, but it is worth pausing to ponder how policy will react. That means stepping into the murky world of politics.

In as much as Budgets are ever non-events, that was very much the plan for the one due this March. Rishi Sunak, over the course of 2021, set out a multi-year package for a substantial increase in taxation – via hikes in corporation tax, increases in national insurance and holding down income tax thresholds - over the course of 2022 and 2023. His hope, it seems, was that he had allowed himself enough wiggle-room in his fiscal targets for a pre-election giveaway in late 2023 or early 2024. That script would have allowed for a few announcements of extra money for favoured projects at Spring’s budget but little in the way of major changes in the overall fiscal package.

Over the coming ten or so weeks the Chancellor will come under pressure to rewrite this agenda.

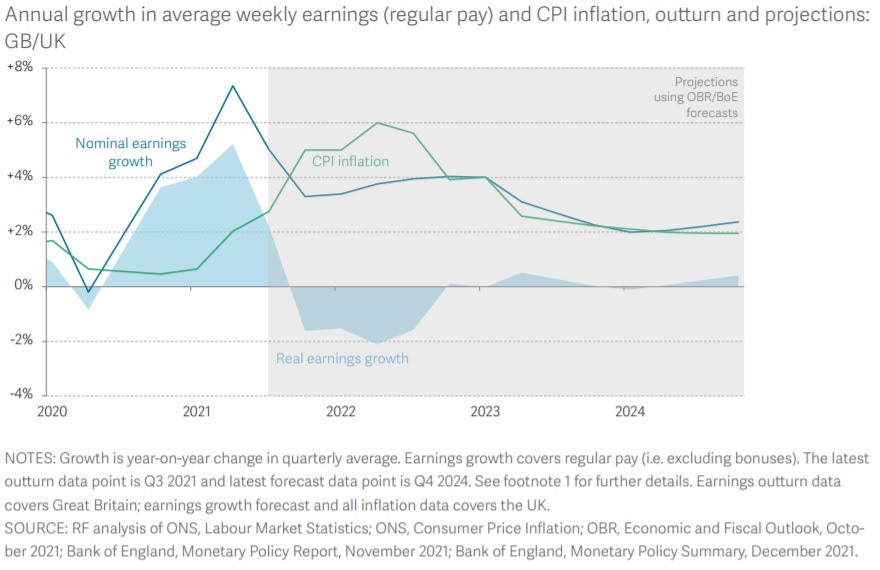

The real income squeeze looks set to be vicious.

The Resolution Foundation have crunched the numbers using the Bank of England’s and the Office for Budget Responsibility’s forecasts – although the consensus of independent economists now points to higher inflation than either official institution expects.

It is striking how quickly the mood has changed. Only a few months ago commentators – and government spokespeople – were falling over themselves to talk up the prospects of strong wage growth. It always struck me as strange to be talking of a rebirth of labour bargaining power – whether apparently caused by Brexit or the pandemic – when real incomes looked set to fall rather than rise over the coming months.

The timing of the squeeze is especially poor for the government. April is set to see national insurance contributions rise, taking a direct bite out of take-home pay and a steep increase in energy bills as the retail price cap is reset. The average household is looking at something in the region of a £600 annual increase in their utility bills.

It’s not only households that will feel the squeeze. VAT on domestic energy is charged at 5% vs 20% on most spending. The more households are pushed into spending on energy, rather than VAT-able expenditure, the less tax rich that spending is for the Treasury.

A big tax rise and a spike in energy bills is hardly the ideal set-up for May’s local elections. Especially when Labour have built up a substantial polling lead.

If the government wanted to smooth the hit to household incomes, there are steps available – but none of them come cheaply or are especially easy. The national insurance increase could be postponed for a year but at a cost of around £12.7bn of extra government borrowing in 2022-23. The government could seek to stagger the cost of rising energy bills by subsidising energy consumption in the short term but again the costs are large – the total increase expected is in the region of £20bn. The mooted call to cut VAT on domestic energy from 5% to 0% would barely be noticed amidst a 50% increase in underlying prices. The most straight forward way to protect low-income households (who typically spend a higher proportion of their income on energy bills) would be an increase in universal credit, but that would look like a U-turn after last year’s unwinding of the £20-a-week pandemic uplift. With that option off the table the government seem to be looking at a major rejigging of the Warm Home Discount. on which I strongly recommended the below thread.

How meaning such a step will prove to be will depend on how much additional borrowing the Treasury will allow.

The fundamental problem for the government – which also complicates any attempt to understand the likely path of fiscal policy – is that the political and economic cycles have been knocked out of alignment by the pandemic. In a counterfactual world in which the pandemic never occurred and I found distinguishing 2020 and 2021 as separate years easier, then fiscal policy would no doubt have been tighter in 2020 and 2021 and gradually eased over 2022 and 2023 setting up a pre-election feel good factor. Instead 2020 and 2021 saw extraordinary measures taken to shield households and firms from the impacts of the deepest fall in output in centuries. And having absorbed the fiscal costs of the pandemic via a twenty or so percentage point leap in the ratio of government debt to GDP in 2020 and 2021, the Treasury is in no mood to absorb the costs of the post-pandemic adjustment. 2022, on current plans, is when households will feel the pain that has been delayed for two years.

It is inconceivable that the government will take no action at all. But, unless the internal dynamics of the Conservative Party dramatically shift in the coming weeks, the action is likely to be not up to the scale of the squeeze.

It is not only the political and economic cycles that have fallen out of alignment but also the incentives of the Prime Minister and Chancellor. Boris Johnson has had a difficult time since the late Autumn. A serious reversal at May’s local elections could see his leadership ended. Viewed from Number Ten Downing Street the imperative is to get through the next few months and hope things turn up afterwards. For the Chancellor, and increasingly many others in the Party, the payoffs look different. Given how the government’s (largely self-imposed) fiscal targets operate, the more fiscal largesse doled out this Spring, the less room there will be for giveaways in 2023 and 2024. A Prime Minister with plenty of political capital to use would surely strong-arm his Chancellor into a more expansionary budget this Spring. But Boris Johnson’s political capital is looking rather depleted.

If you’re enjoying Value Added please do consider subscribing. You’ll get more posts and I’ll get the resources to carry on producing it.

I was originally intending to increase the price of a subscription on January 1st (for new subscribers only, existing subscribers will stay at the same price they are already paying) but I forgot to schedule it decided to not immediately add to the cost-of-living squeeze. The price increase, for new subscribers, will now come in on the 1st February. So take advantage while you can.

inflation!