We fell off the cycle

Getting back on will take a while.

On one level understanding UK macro at present is remarkably simple: demand has recovered faster than supply. As restrictions have eased and confidence has returned spending has picked up relatively sharply. But the supply side of the economy is still struggling with the impacts of both the pandemic and Brexit. The result has been series of production bottlenecks, logistical holdups and a rise in inflation. In recent weeks the job of a British economics correspondent has mainly been reporting on what seems to be an ever-changing carousel of shortages. Much, but not all, of the supply side disruption should ease over the coming 12 months. Policymakers would be well advised to remember that patience can be a virtue and to look through the spike in inflation.

But economists and economy-watchers like to make things more complicated. The question they often want to pose is “whereabouts in the business cycle is the economy?”. Monetary and fiscal policy hawks are wont to point to the rising rate of inflation and the difficulties some firms are having in hiring and conclude that the economy is not only reaching the later stages of the cycle but is in serious danger of overheating. Some analysts seem to have switched from an ultra-pessimistic view of a semi-perpetual slump to an almost equally pessimistic view of a coming inflationary spiral with barely a moment to catch their breath.

The better answer the question of “where in the business cycle is the British economy?” is “we fell off the cycle sometime ago and are in the process of getting back on it”.

The recession that hit in 2020 was not a normal recession. Not only was it the deepest Britain has experienced in its modern economic history, but it was also one of the briefest. It was caused by a truly exogenous shock. Recessions do not typically happen because the government orders people to stay at home and businesses to pull down their shutters.

Just as the recession was not normal, nor is the recovery. Modern economies are not simple things that can be turned on and off like a light switch. And while that might sound obvious, it is all too often missing from the discussion of the current outlook.

The key thing to understand is that the lockdown-related turbulence of 2020 and early 2021 did not just suppress demand, it reshaped it. And supply reorganised itself in response. In important ways the economy has been twisted out of shape and is now in the process of unbending itself. That process is proving far from smooth.

Understanding where the British, and many other advanced economies are today, means keeping in mind that this process is ongoing. Data releases should be seen in the context of a pandemic-driven business cycle rather than a traditional one.

Take retail sales as an example. In August they dipped, in volume terms, by 0.9% month on month compared to July. Cue much gnashing of teeth from people worried about a recovery losing momentum. Certainly, falling retail sales in the early stages of a typical recovery would usually set off more than a few warning lights.

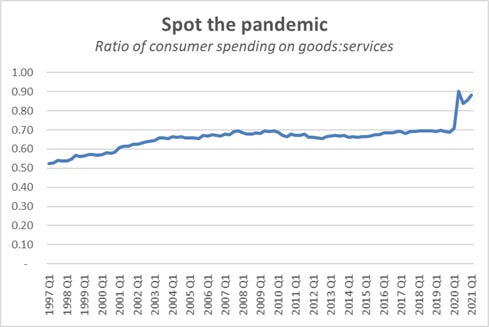

But this is not a normal recovery. Last year saw an enormous shift in consumer spending away from services and towards goods. The typical Briton consumed fewer calories in restaurants and cafes and bought more from supermarkets. They went to the pub less often and used Amazon a lot more.

Over the course of 2020 consumer spending on services fell by 16% while consumer spending on goods rose by 4%. That led to a dramatic shift in the usual ratio of household spending on goods vs services.

Indeed, by April this year non-fuel retail sales were almost 13% above their pre-pandemic level even while GDP was still 3.7% below its pre-pandemic peak.

As the hospitality sector has gradually re-opened, indoor leisure activities have resumed and consumer focused services firms have begun trading again, the great goods shift has begun to reverse.

Falling retail sales since April are not a sign of a consumer downturn but part and parcel of a normalisation in household spending.

That is not to say though that August’s weak retail numbers are nothing to fret about. Just that they are not as concerning as they first appear. Real time indicators of consumer spending on services – whether that is restaurant bookings at OpenTable or the mobility data supplied by the tech firms – point to a general economic soft patch over the summer. The spike in covid-19 cases in July hit both the supply and demand sides of the economy and much of that weakness seems to have bled through into August. The September case numbers are not encouraging.

To state the obvious again: in the pandemic-business-cycle the course of the virus will have a serious effect on output levels, the volatility of monthly GDP prints will remain higher than normal.

If you’re enjoying Value Added, please do share it.

Excellent first post. Thank you! If the volatility of data is high, is this more like a 80/90s data cycle in terms of characteristics? Will market participants, who have become accustomed to a smooth data path, have to continually adjust expectations for the policy path or do you expect firmer policy guidance?