What does Omicron mean for the economy?

The short answer is more uncertainty. What matters is not so much government rules but consumer behaviour and that is harder to forecast.

A recurring theme of this newsletter has been that we are not experiencing a normal recovery. This business cycle is still, to a large extent, pandemic driven. The discovery of the Omicron Variant has provided a reminder that the pandemic really isn’t over.

In the spirit of Value Added, there is very little point in me speculating on the epidemiology of this new strain. But the economics of it clearly matter.

The consistent line from the epidemiologists now is that it too early to tell how Omicron will play out. The uncertain path of the virus makes the path of the economy equally uncertain, and I suspect it is that uncertainty which has driven sharp falls in risk assets. The one thing we know now is that we won’t really know anything for a couple of weeks – and in that environment, especially so close to year end, it makes perfect sense for asset allocators who can reduce risk to do so. I find it hard to read more into recent equity market moves than that.

Even amid the uncertainty though, the early consensus appears to be that the new variant is a negative for the global economy but perhaps not a huge one. I am a bit less optimistic. The recovery might indeed shrug Omicron off, but the downside case is clear.

Working through the impact on the British economy is instructive and brings home how uncertain the situation is.

As Julian Jessop set out in a useful Twitter thread, the material impact of Britain’s new restrictions should be small.

Mask wearing in shops and public transport shouldn’t have any noticeable impact on spending. The new international travel rules – a PCR test within two days of arrival followed by 10 days of isolation if positive coupled with a tougher approach to visitors from Southern Africa – may deter a few business travellers and tourists, but again this should be relatively small in the context of overall GDP.

The requirement to isolate for ten days, regardless of vaccination status, if you come into contact with an Omnicron case is potentially a bigger deal. This an effective return to the pre-mid August rules and may see a repeat of the “pingdemic” of July with potentially tens of thousands of workers having to isolate each week. That’s clearly a negative for the economy’s productive capacity but, again, a manageable one.

Even if the restrictions were to be tightened from here, the economy has adapted to lockdowns.

The ultra-bearish case of a repeat of the kind of restrictions imposed last Spring – which feels far from likely - would not see the same kind of collapse in GDP witnessed then. April 2020, to paraphrase TS Elliot, was the cruellest month. GDP fell by almost 19% on the month before.

But by the third lockdown, which began in late December 2020, the economy had adapted. Manufacturing and construction activity, much of which closed in Spring 2020, maintained more output. More retailers managed to switch their business from the high street to online. Many more hospitality business operated a take-away trade. Faced with similar restrictions to the first lockdown, firms did a much better job at sustaining output levels.

So far, so reassuring. But the uncertainty over the outlook for the coming months comes not so much from government actions as from consumer behaviour. The new rules are clearly designed to minimise restrictions on the social-contact intensive hospitality sector ahead of what is traditionally their busiest trading season.

But it is easy enough to see a scenario where, whatever the official rules say, there is a pick-up in voluntary social distancing. People may well choose to forego trips to the pubs and restaurants either to avoid potential infection or, just as likely, to avoid contacts that will force them into ten days of home isolation.

Headlines about a new variant and the return of covid-themed government press conferences could have a chilling effect on consumer confidence. It is worth remembering that such voluntary distancing began well before the formal lockdowns in March 2020.

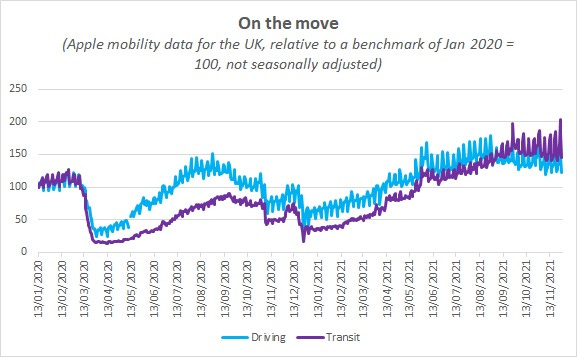

The first national lockdown was imposed on 23 March 2020, following the Prime Minster urging people to avoid non-essential contacts on 16 March. But between the beginning of March and that plea for restraint, transit usage and driving (according to Apple’s mobility data) had already fallen by around 20-30%.

The real economic risk in the coming weeks is a repeat – perhaps on a smaller scale – of that kind of (entirely rational) behaviour.

The early consensus seems to have pegged such behaviour as disinflationary. I am not so sure. Yes, it would involve weaker spending – relative to the path expected a few weeks ago, even if not in absolute terms (it is almost Christmas after all) – on consumer services but higher spending on consumer goods. Given the drivers of the recent higher inflation, I struggle to see how more demand for consumer goods would do much to dampen it. I am afraid for the moment, the best thing to do is watch the mobility data and try to gauge if, and by how much, consumer behaviour is switching.

If you’re enjoying Value Added please do subscribe. You’ll get more posts and I’ll get the resources to carry on producing it.