Fiscal rules & fiscal vibes.

When it comes to fiscal credibility, vibes matter.

I’ve never been entirely sure what the point of British fiscal rules is.

In theory they are supposed to safeguard against the tendency of politicians to run up too much debt by setting out the conditions under which public borrowing is seen as appropriate. This should, again in theory, lower borrowing costs over the cycle as whole. A credible commitment to a prudent approach – to dust off an old favourite phrase of Gordon Brown – should, as the IFS put it in 2021, make it harder for governments to borrow for bad reasons but easier and cheaper to borrow for good ones.

But that theory does not appear to translate especially well to the reality of the last decade and a half or so of British macro-policy.

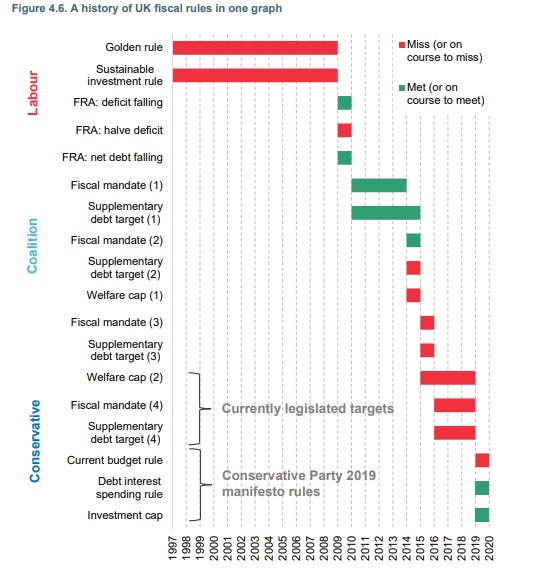

A look back at British rules since 1997 by the IFS found two things. First, they have been chopped and changed pretty frequently – especially in recent years – and secondly: they were more often missed than hit.

It is hard to look at this list and conclude that such rules have ever been especially binding. And if the commitment is not binding, it is hard to see much benefit from it in the way of lower borrowing costs.

Since 2010 fiscal rules in Britain have more often served a political than an economic purpose. For much of the 2010s questions about government debt and deficits consistently polled amongst the top issues facing the country and fiscal rules were a useful way of politicians signalling their stance to the voting public.

In an odd inversion of the usual logic of economics textbooks, the markets seemed more relaxed about British government borrowing than the general public.

Fiscal rules are supposed to guard against a deficit bias that comes of the general public being keen on voting for politicians who promise them tax cuts and spending rises and put off the difficult choices. In the 2010s, it was hard to find evidence of such a bias among the voting public. The party promising to take the tougher approach to the deficit was consistently re-elected. Meanwhile the yield on gilts plumbed new lows as markets snapped up any safe assets available.

Now though things seem to be changing on both accounts. Public concern about the deficit and government debt has evaporated and been replaced with worries about energy bills and inflation. But the markets are showing some signs of concern.

In an environment of high inflation, rising interest rates and heightened uncertainty fiscal rules may matter more than they have for a decade or so. Whereas before they served as useful tool for political signalling, there may now be some actual need to appear credible to financial markets.

Kwasi Kwarteng is due to sketch out his own fiscal approach this week. Although we may have to wait for a full budget later this year to get the full picture.

There is no such thing as a perfect set of fiscal rules. Most observers would agree that, in normal times, it makes sense to balance the current budget so that borrowing is only for either long term investment or short-term countercyclical policy. But the timeframe over which to aim for a current budget balance is hard to get right. Set the target too short and it forces unnecessary pain on public services and household income by over tightening policy, set it too long and it gives policymakers far too easy an opportunity to simply change the rules before they bite.

…the Chancellor will need to outline clearly his fiscal principles, so the market understands the commitment to fiscal discipline through reducing the ratio of debt to GDP. Markers may need to be laid down to guide the market’s thinking.

I can certainly see the benefits of such an approach. It has the advantage of both being clear and sufficiently medium-term that there will be less need to chop and change it in the short run.

Of course, it this raises some rather large questions, not least about what sort of level of debt/GDP the government will be targeting? And over what time frame?

The more fundamental question though is not about what fiscal rules Kwarteng will adopt but whether it will make any difference in the near term?

The simple facts are that the government has announced a fiscal intervention in the energy markets that may cost in the region of £100bn in the coming year. They look set to follow that up with £30bn or so of discretionary tax changes without an accompanying forecast from the Office for Budget Responsibility. There is at least an even chance that there will be discretionary tax cuts that go beyond the already widely signposted moves in national insurance and corporation tax. It is hard to know what one could say alongside side such acts. Actions tend to speak louder than words.

A few weeks ago Janan Ganesh wrote up his vibes theory of politics in the FT. I’m not so sure about politics but vibes definitely matter when it comes to fiscal credibility.

Take George Osborne. He missed most of his fiscal targets. He changed them with surprising speed. The ratio of government debt to GDP rose by about ten percentage points during his time as chancellor. But his vibe? Fiscally conservative, tough, prepared to take ‘difficult decisions’.

His own first fiscal act was an emergency budget which cut public spending and tightened the fiscal rules he inherited. By contrast the first time Kwarteng is at the dispatch box he will be outlining a radical loosening in the fiscal stance and setting out a relaxing of the fiscal rules.

The vibes will be very different.

Thanks for reading Value Added. It is a subscriber funded publication. If you’re enjoying it please do consider taking out a subscription. You’ll get more posts and I’ll get the resources to carry on writing it.