Omicronomics: the fallout.

Britain's omicron wave seems to have peaked. Real time data allows a quick assessment of the damage. Outside of hospitality it looks limited.

Britain’s omicron case-wave appears to have peaked. Given the lag between cases, hospitalisations and deaths it’ll be a little while before the full health impacts are known but the worst of the economic damage is now hopefully behind us.

A full assessment will have to await the hard data from the Office for National Statistics but the real time data gives some early clues.

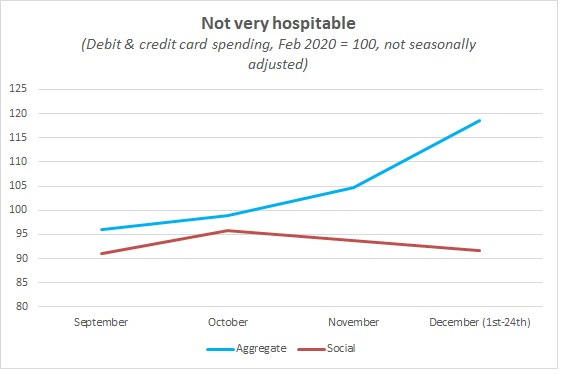

The CHAPS data published by the ONS gives a decent steer on how consumers reacted to spiking cases. Whatever the official rules said, it seems many responded in a perfectly rational way by minimising social contacts to avoid being stuck self-isolating over Christmas.

The data requires careful handling. For a start it is not seasonally adjusted and consumer spending displays large seasonal patterns. And, most frustratingly of all, the series is only available back to the beginning of the pandemic, so it is hard to see what a “normal” year should look like.

In the chart above, I’ve used monthly averages for the aggregate (i.e. total) and social categories for September, October and November but used the data for the 1st to the 24th for December. My reasoning being that a post-Christmas immediate seasonal slump in spending for a few days should be expected.

There is no doubt that the hospitality sector had an awful Christmas. Spending levels were lower than in November and materially lower than in October. In the run-up to Christmas, the overall level of consumer spending on social activities was around 10% lower than the month before the pandemic. But even that is an understatement – February is not known as an especially busy month for the pub and restaurant trade. Hospitality bosses reckon that in a pre-pandemic year, December volumes would typically be around 150-180% of February levels.

Almost as interesting as the relative hospitality slump, has been the strength of total spending. Again, perhaps not as much as in a normal year, but still notable. Consumers reacted to the omicron wave as they did previous ones: by dining and drinking out less and buying more goods.

That is certainly consistent with the latest update from the British Retail Consortium, showing a strong close to the year for retailers.

· On a Total basis, sales increased by 2.1% in December, against a growth of 1.8% in December 2020. This is above the 3-month average growth of 2.8% and the 12-month average growth of 9.9%.

· On a two-year basis, Total retail sales grew 4.6% (Yo2Y) during December compared with the same month in 2019.

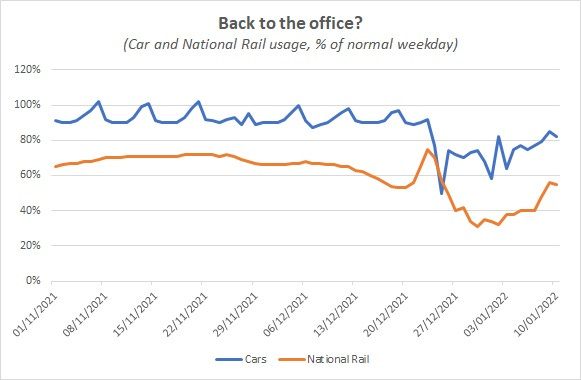

If the avoidance of busy places was driven by a desire to avoid isolating over Christmas or infecting elderly relatives, then it should, in theory, reverse quite quickly. There is already early evidence that this is happening.

While the “Plan B” guidance in England suggests that working from home (where possible) should continue until late January, the latest data on transport usage points to a steady return to the office.

The real time data has its limitations but points to a relatively small overall hit to the economy from omicron and a much larger and more concentrated blow to the hospitality sector.

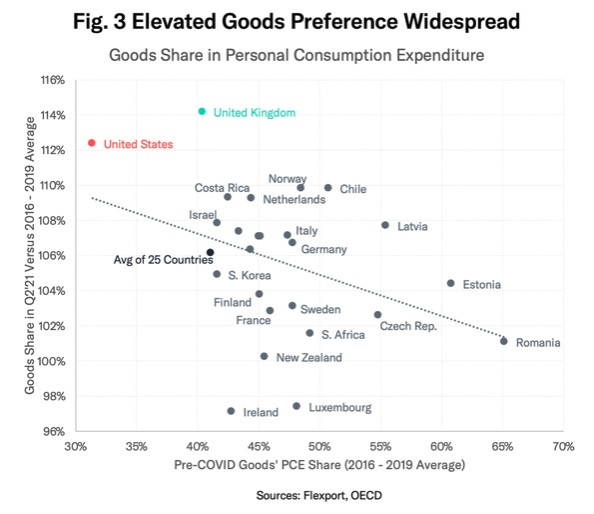

The latest wave of the pandemic seems to have, once again, increased demand for goods relative to services and, as a consequence, probably added a touch to inflationary pressures. On which note, this chart from Flexport is especially striking:

Despite the relatively limited economic fallout from omicron, the mood in consumer-facing sectors, even outside of hospitality, feels pessimistic. The BRC may have reported a decent end to the year but the forward-looking statements struck a grim tone.

…retail faces significant head winds in 2022, as consumer spending is held back by rising inflation, increasing energy bills, and April's National Insurance hike.

And one should probably add the gradual impact of Bank of England tightening.

Squeezed consumers make for a tough trading environment.

If you’re enjoying Value Added please do consider subscribing. You’ll get more posts and I’ll get the resources to carry on producing it.

I was originally intending to increase the price of a subscription on January 1st (for new subscribers only, existing subscribers will stay at the same price they are already paying) but I forgot to schedule it decided to not immediately add to the cost-of-living squeeze. The price increase, for new subscribers, will now come in on the 1st February. So take advantage while you can.