The Bank of England can turn a mistake into an opportunity.

Changes in the housing and mortgage markets over the last two decades have changed how British monetary policy works. That sets up an interesting opportunity for the Bank of England.

Filling the column inches ahead of the Bank of England’s meeting on Thursday can be tricky. There are only so many times one can write “will they or won’t they hike?”. The Telegraph’s business pages this week alighted upon a novel alternative by digging through documents at the Land Registry to produce the headline “Top Bank of England rate-setters insulated from higher mortgage costs”. It seems that neither Andrew Bailey, nor his “key lieutenants”, have a mortgage.

Mr Bailey’s own housing tenure is not especially relevant to monetary policy but the fact that he is far from atypical is rather more interesting. Patterns of home ownership have changed radically over the last couple of decades with potentially important implications for how the monetary transmission mechanism works.

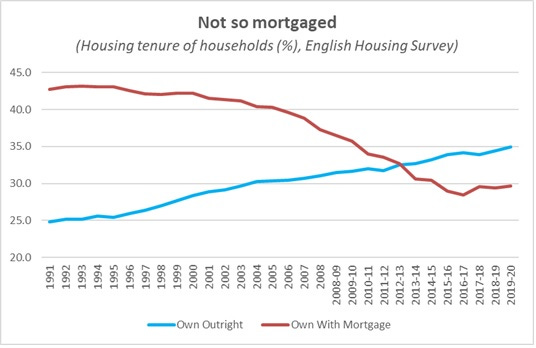

Firstly, there are simply fewer mortgagees about1.

Since 2011/12 there have been more outright owners of homes than mortgaged households.

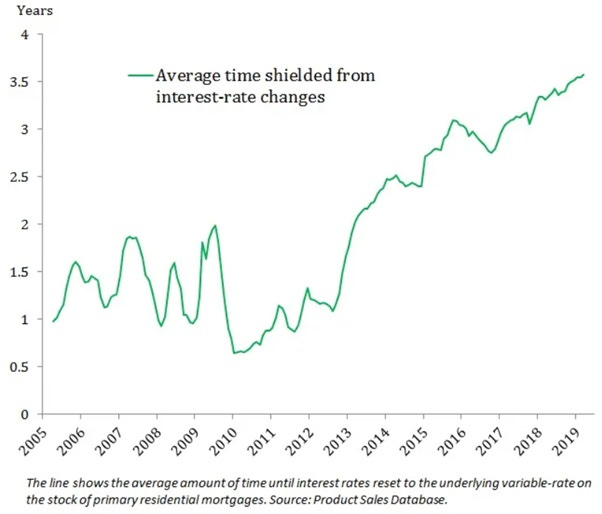

And secondly, those holding a mortgage are much more likely to be on a fixed rate than in the past.

According to the Financial Conduct Agency over 90% of mortgages taken out in the last five years have been on a fixed rather than a variable rate. By contrast, as recently as a decade ago over 60% of UK mortgages were on a variable rate.

An excellent analysis by the Bank a couple of years ago demonstrated that, as of late 2019, it would take around 3.5 years for any change in Bank Rate to feed through into the monthly mortgage costs of the median mortgage borrower.

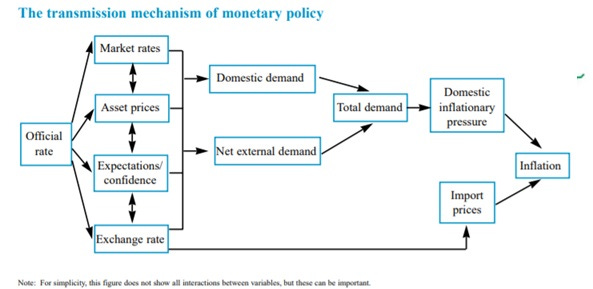

This is all a world away from the description of the housing market found in the Bank’s 1999 article on the transmission mechanism of monetary policy.

… most mortgages in the United Kingdom are still floating-rate. Any rise in the mortgage rate reduces the remaining disposable income of those affected and so, for any given gross income, reduces the flow of funds available to spend on goods and services. Higher interest rates on unsecured loans have a similar effect. Previous spending levels cannot be sustained without incurring further debts (or running down savings), so a fall in consumer spending is likely to follow.

The combined impact of fewer households holding any sort of mortgage at all and those that do hold them switching to fixed term deals is substantial. Twenty years ago, any change in Bank Rate would have an immediate impact on the monthly housing costs of approximately 25% of all households. If the Bank does hike this Thursday, fewer than 5% of households will feel a similar impact.

Of course, there is more to monetary policy transmission than the direct, and immediate, impact on household cashflows. The Bank’s 1999 stylised chart is a useful framework.

The “market rates” to “domestic demand” feedthrough may be weaker than in the past but the Bank will be hoping that other channels will compensate for this2.

The changing nature of the housing market perhaps explains much of the Bank’s shift in recent years towards talk of the importance of expectations.

The problem with this approach, as I’ve written recently, is that it is hard to get right. Done badly it leads to situations such as this:

So where does this leave the MPC heading into Thursday’s meeting?

In a potentially interesting place. 15 or 20 years ago much of the impact of British monetary policy came through the direct effects of changing interest rates on household cashflows, nowadays though the actual change in Bank Rate is less material and expectations about the future path of Bank Rate play a larger role.

The mechanical impact of raising rates from 0.1% to 0.25% either this week or in December is really neither here nor there3. The bigger issue is that, listening to the hawkish noises coming from Bailey and Pill, the market has moved to price in not just a hike to 0.25% but a reasonably steep and rapid tightening path over the coming 18 months.

I continue to think that allowing expectations to run so far was a mistake but there is now, at least, the potential to turn that mistake into an opportunity. If the Bank hikes to 0.25% either this week or the following month whilst clearly explaining that the tightening cycle which will follow will be at a slower incline than the market currently expects then it can deliver that favoured oxymoron of rate commentary: a dovish hike.

If you’re enjoying Value Added please do subscribe. You’ll get more posts and I’ll get the resources to carry on producing it.

I am using the English Housing Survey rather than the ONS’s UK-wide data as the EHS is timelier.

The MPC will no doubt be reassured by this 2016 paper which looked at the impact of rate changes in the UK and US (with their (then) very different mortgage market structures) and concluded that the general equilibrium effect of monetary policy on household income mattered more than the direct effect on cash flows.

I am assuming the first hike will be 15 basis points to get them back on the familiar 25 basis point increments.